Are we in a Housing Debt Bubble ?

Property purchase is a very hot topic of discussion among Family/Friends. Some feel purchasing a house is a good investment even on loan ( most actually) and there are others who feel staying on rent is a much better choice for a young Investor.

I personally have always believed in staying clear of any kind of loan. Be it personal or home loan. Let’s see how good/bad an idea it is to purchase a house on loan. For a young Investor taking a Home Loan would be probably the only option. If bought with cash then it is a better investment ( if land on your name is part of the deal )

It’s the land that appreciates over time and never the concrete block that stands on it.

Everyone these days is paying exorbitant rates for an apartment believing its a great investment. Take Mr.Homie our energetic young investor who decides to purchase an apartment for various reasons ( peer pressure, emotional family blackmails, false investment promises …. ) . We shall break down his adventures of buying a home into several stages.

The misadventures at Housing Mela’s

Mr.Homie visits one of those housing Mela’s with his friends/family just to get a taste of what’s new in the housing market. Unfortunately, Agents at the Mela flock to him like ants to sugar in summer. Agents are paid by the number of scapegoats they can trap and introduce him to several so-called dream projects currently available from the best builders in town. The dream projects are 2BHK apartments which cost “just” 80 Lakhs in “Prime” locations.

There is a swimming pool, tennis court, basketball court, play area. The total apartments are “just” 200 in total. There is enough space in the pool even if 1/10th of the residents decide to swim at the same time on a given day,which is not true :P.

Some even have buses parked outside that will take you on a free tour of the apartment complex !

The Prime location and just Syndrome

Every apartment complex is located in Prime locations as per the builder, they are a hop away from everything measured in Kilometres(km) !

- Just 3kms from the upcoming metro station

- Just 4kms from multiplex/mall

- Just 3 km from IT Park

- 5 international schools in just a radius of 4kms

- And just 100 meters from the cemetery, which they don’t mention for obvious reasons.

Unless your apartment is deep down in a forest, it would mostly satisfy all the above Prime location requirements.

Mouthwatering Loans

The Agent at the Housing Mela now points out the special Loan/EMI schemes that will expire this month ( sometimes only valid for the day) and might never come Mr.Homie’s way. Mr.Homie hardly gives a nod and within no time the apartment papers are ready, 50L loan pre-approved for 20 years tenure, a gold coin, a dish connection ( for which u need to pay the rentals). Last but not the least a box of sweets for close to diabetic friends at workplace and a small party to your close family and friends to justify and feel happy about the accomplishment. All this for a sign on some papers!

How many of you or your family members/friends have narrated this too good to be true stories. Most are in cloud 9 with the thought of having an own house at such a young age!

Debt = unknowingly selling your soul to the devil.

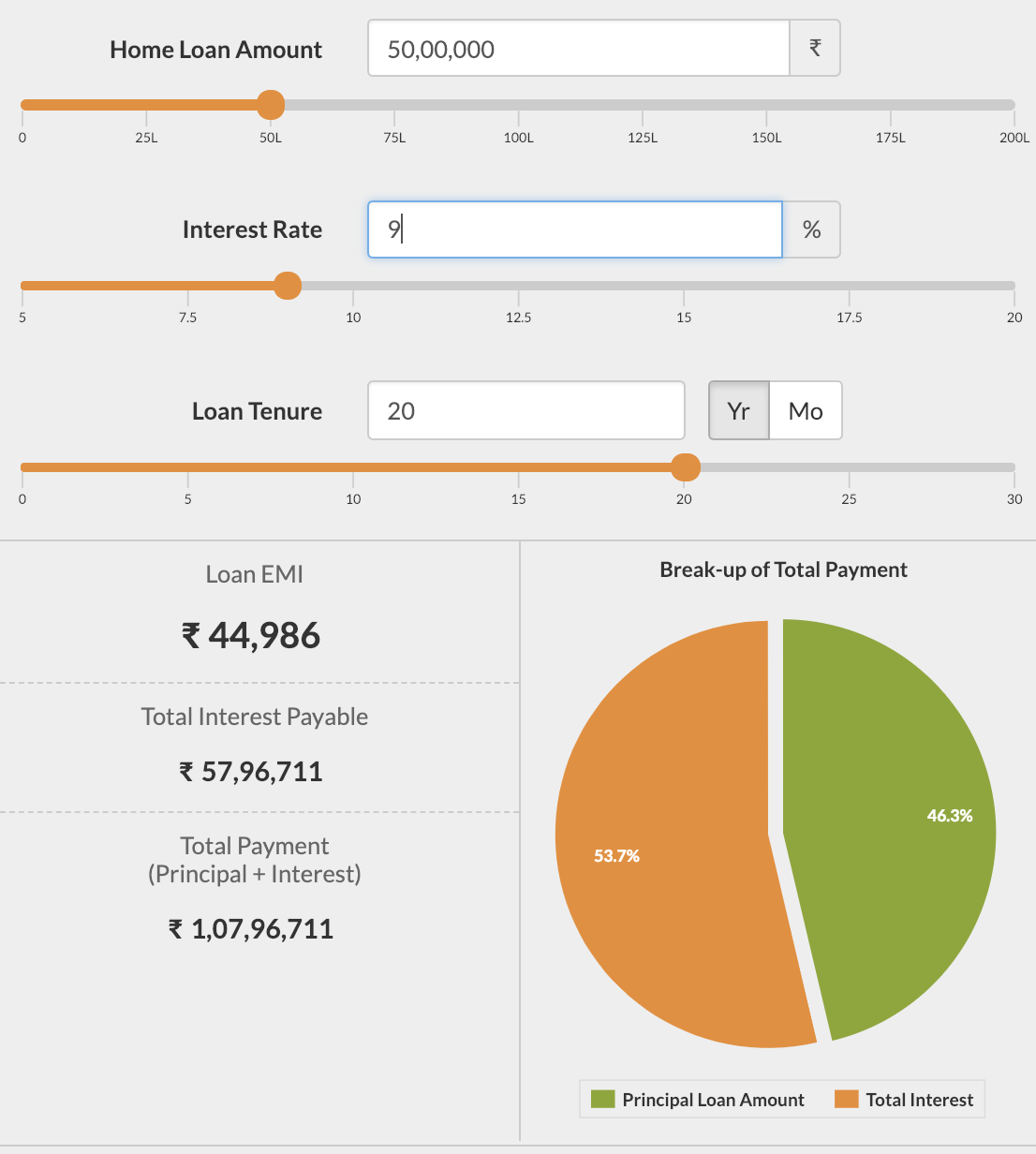

Let’s open our eyes to the harsh reality and see how good an investment mess Mr.Homie has got himself into. Mr.Homie took a home loan of 50L. How much do you think he will be paying in interest at 9% ( as of Jan, 2019 ) for a tenure of 20 years?

Mr. Homie would have paid a whopping 57.96 Lakhs in Interest alone ! Let’s do some simple math to see the total cost.

| Apartment Expense | Cost in INR |

| Base price of an apartment | 30L cash + 50L Loan = 80Lakh |

| Interest amount paid on the loan | 57 Lakh |

| Maintenance of 5K/month increasing at ~5% | 20 Lakh |

| TOTAL cost + expense | 1.57 Crore |

Mr.Homie just paid 1.37 Crores for an apartment that had an MRP of 80 Lakhs. Add to this the maintenance charges that need to be shelled out every month. Assuming it to be 5K , at an increase of 5% over the period of 20 years would be another 20 Lakhs.That’s brings the cost of Mr.Homie’s apartment to around 1.57 crores at the end of 20 years.

Mr.Homie has a friend in the same apartment and boasts how good an investment it was 20 years back. Their apartments are now priced at 1.6 crores each in the market, a very good return for their investment.

1.6 Crore is just a hypothetical number.Forget 20 year old apartment, You cannot find buyers for a 10 year old apartment these days !

By now we might have understood what Mr.Homie has landed himself into 😕. Not just that , assume Mr.Homie with luck finds a buyer for his 20-year-old ancient apartment at 1.6 Crores. He signs the papers after 20 years “again” with tears in his eyes ( for that emotional attachment with the home, unfortunately not that he has lost money ).

20% Capital gain tax on long term returns needs to be paid even on the interest amount paid as part of loan. One cannot take double tax benefit on the loan amount ( most show the loan to get tax rebate ). Its a big trend in India these days to avail home loan for tax benefits

.

Luckily it is calculated on the Indexed Cost of the Property.

How much did Mr.Homie gain in the sale?

Before we calculate the profit and capital gain tax we need to understand CII ( Cost Inflation Index ) .

Cost Inflation Index is an index used to factor in the effect of inflation in the prices of Capital Assets. CII is used while calculating long term capital gains.

In order to calculate capital gain on sale, we need to calculate the Indexed Cost of property( ICOP )

ICOP = APP * ( Index in year of sale / Index in year of Purchase )

where

APP = Actual purchase price

ICOP = Indexed cost of property

In general, the CII ratio for 20 years is around 2.5 ( see CII here ). If a property is bought for 10,000/- and sold in 20 years for around 50,000.

The Indexed cost of the property would be

10,000 * ( 2.5 ) = 25,000/-

The capital gain would be

50,000 – 25,000 = 25,000/-

on which capital gain tax of 20% has to be paid ,which is 5,000/-.

Indexed cost of property is calculated to account for inflation. CII is decided by income tax department every year

| Apartment Sale | Cost in INR |

| Purchase price of apartment | 80L |

| Apartment sold at | 1.6 Crore |

| Indexed Cost of Property | 80L x 2.5 = 2Cr |

| TOTAL Profit | 1.6 Cr – (2Cr) = – 40 Lakh |

Mr.Homie has made a profit of around 3 lakh ( 1.6Cr – 1.57Cr) in cash and on paper lost 40 Lakh in the span of 20 years.Of course he can claim the 40 lakh as loss to Income tax Department over the next several years 🤦♂️.

If Mr.Homie had wisely invested half the EMI for 20 years ,it would have built him a huge cash chest of 2Crore + . – Read 20K rule

In Mumbai, this would still make sense due to lack of land. In a city like Bangalore every year a remote village gets added to it. The appreciation of the apartment as an asset has stagnated.

The owner does not own a piece of land directly when he/she owns an apartment ( its society owned ).

Nearly 50% of the newly constructed apartments are empty ! When you hear a radio ad telling you about only a few more apartments left… think of it logically.. If there were only a few left, why would the builder waste his money giving ads on Radio and newspaper 😉 .

Standard of Living takes a deep dive…

Mr.Homie would have initially showcased his brand new shiny apartment to everyone in his family/friends, but soon has to cut down on all expenses just to clear his loan. Some “smart” people will take a personal loans to compensate for the cash crunch they are facing.

The loan is somehow lately the new answer to all financial problems. Not far ago, taking loan was a taboo. Anyone taking a loan was considered a fool who did not know how to manage his/her finances. Not anymore… Flaunt a brand new car, bike, vacation and whatnot, all on loan, post them on Facebook, Twitter, Instagram. Wait for likes, Life is beautiful !!

Stay clear of Debt

I am not saying never to buy an apartment. Just think twice before committing to one and definitely not on a loan. Debts are a downward spiral hard to come out of. By the time Mr.Homie has cleared his debt and “settled” in life, there is hardly any fund left for retirement. He can’t even sell the apartment as moving into a home on rent hurts his ego ( also the loss that will be incurred ).

Paying the Landlord vs the Bank!

Decide which one do you prefer , paying 25k for a 2BHK or 70k to the Bank as an EMI for the same 2BHK. The choice is yours !

Instead, build your Freedom Fund and stay in a rented house unless you can afford to buy one. Wait for the market to crash, the current prices are exorbitant and the Housing bubble is waiting to burst just round the corner. With just half the amount invested smartly , you can retire with a lot more money and happiness. Having money to spend on things you need is more important than an old worn down apartment and nothing to spend on for a decent living.

At just 20K per month you can build a cash chest of 2 Crore ! – read the 20K rule

Save your money wisely. Housing bubble or not, Debt needs to be avoided like the plague! Unless you plan to make an income out of the Debt, there can be good debt too “sometimes”…

If the idea is to buy a house as an investment to yield rent, think again. A decent 2bhk house assuming costs 1Crore and the rent you plan to yield from it is 25,000/- . That makes it a measly return on investment of 3%. Not accounting to the fact that maintenance charges on an aging property goes up every passing year.

Please read the disclaimer carefully before making any investment based on the articles published on this Blog !!

One response to “The Housing Debt Bubble”

[…] I personally feel Home Loan is never the way to go for building your Freedom Fund. Talking about the return and tax benefits on Home Loan would be like committing a crime for me ! Everyone is entitled to their opinion and mine is jotted down in this article ( Housing Debt Bubble ). […]

LikeLike